Investing in Qualified Opportunity Zones

Investing in Qualified Opportunity Zones

Summary: Qualified Opportunity Zones (QOZ) allow gains to be reinvested in certain under-developed areas with three potential benefits to the investor. First, the tax on the gain is deferred until 12/31/2026 (payable in 2027). Second, if the investment is made before 12/31/21, 10% of the gain is eliminated for tax purposes. Third, any gains on the investment in the opportunity zone are tax-free, as long as certain conditions are met. A fourth benefit pertains to holders of depreciated investment real estate only - any straight-line depreciation taken on rental property will be tax-free if held for the minimum ten-year requirement. These benefits make Qualified Opportunity Zone investments very compelling for investors with large unrealized or recently realized gains in high tax brackets.

Background:

One of the new tools in the Tax Cuts and Jobs Act of 2017 (TCJA) is the Qualified Opportunity Zone. The purpose is to attract investment in lower income areas to create jobs and catalyze economic growth.[1] Rather than a top-down government program where taxpayer money is allocated through a political process, the philosophy of the opportunity zone provisions is to provide investors with an incentive to invest in under-invested communities of their own choosing and in their own way.

Qualifying Opportunity Zone (QOZ) Investments:

Per the IRS, “A QOF [Qualified Opportunity Fund] is an investment vehicle that files either a partnership or corporate federal income tax return and is organized for the purpose of investing in QOZ property.” QOZ property is owned by the QOF and meets three requirements: 1) acquired for cash after 2017, 2) it is held by a corporation or partnership and is a QOZ business, 3) it remains a QOZ business for 90% of the holding period. The QOZ business must earn at least 50% of its gross income in the QOZ.[2] If the QOZ purchase is for land, it must be “substantially improved” to qualify, meaning the investment basis must be doubled.[3] So-called “sin businesses” are not eligible for QOZ treatment. These include golf courses, country clubs, massage parlors, gambling facilities, and businesses primarily engaged in serving alcoholic beverages.[4]

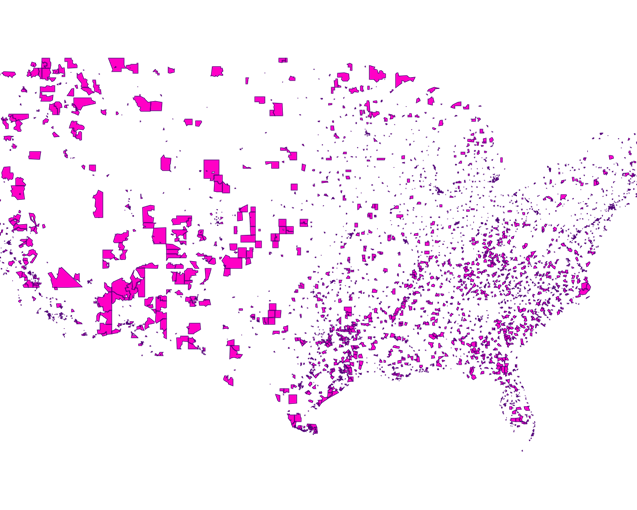

Where are Opportunity Zones?

Per HUD, “Opportunity Zones are economically distressed communities, defined by individual census tract, nominated by America’s governors, and certified by the U.S. Secretary of the Treasury…”[5]

There are 8766 opportunity zones across all fifty states. These zones on average have higher poverty, lower median family income, higher concentration of minorities, lower high school graduation rates, higher unemployment, higher vacancy rates and lower life expectancy than other low-income census tracts.[6] They are in need of investment.

Source: https://opportunityzones.hud.gov/resources/map

What can be invested into a Qualified Opportunity Fund (QOF)?

Any gains can be invested into a QOF and receive the preferential treatment as long as the gains are invested within 180 days of the sale, and the sale was not to a related party.[7] Note that if the gains came from a partnership, the taxpayer has until 180 days after the tax return due date of the partnership for the year in which the gain was realized.[8] A payment from the investment fund in excess of basis would also be an inclusion event. (Note that if you only contribute gain, your basis is 0 until you get the step-up.)

What are the benefits of an Opportunity Zone Investment?

First, by timely investing gains into a QOF, the tax realization of the gain is deferred until the earlier of December 31, 2026, or an inclusion event. In general, an inclusion event is a transfer (by sale or gift) of the QOF interest. These deferred taxes can be invested, essentially creating an interest-free loan from the government. Second, investments made before December 31, 2021 and held for five years receive a “basis step-up” of 10% after five years. This means that if a $200,000 gain (basis = $0) is invested in the QOF before the deadline and held for five years, the basis (or tax-free amount) becomes $20,000. Note that the 5% basis step up at the end of 2025 only applies to investments made before 2021. Third, and most importantly, any gains made on the QOF investment are tax free, as long as the funds are invested for at least ten years.

Source: https://opportunityzones.hud.gov/investors

The fourth potential benefit of a QOF does not apply to everyone, but can be very valuable. Usually, when rental real property is sold, the selling price less the original investment amount is taxed as a capital gain, and the amount that the has been taken as depreciation is recaptured and taxed at ordinary income tax rates. If gains from a rental property are reinvested into a QOF, and held for a minimum of ten years, the gains from depreciation recapture are not taxed at all.[9]

The following case studies demonstrate the potential tax savings from a QOF. Note that the after-tax return is based on what would be the after-tax gain from the funding asset, and that this assumes only the gain is reinvested in the QOF. Further, this analysis considers the value from deferring tax by five years, and assumes that those gains are invested over the next five years, since the tax is due in 2027.[10] These examples grow the negative cash flow from the deferred tax at the same rate as everything else. We see a substantial benefit in Case Study 1, and an even greater benefit in Case Study 2.

Source: Rothman Investment Management calculations.

Source: Rothman Investment Management calculations.

Who should consider Qualified Opportunity Zones?

Anyone with unrealized or recently realized short or long term capital gains should consider investing those gains into a Qualified Opportunity Fund. There are many issues to consider, however. These include: liquidity needs, tax rate, risk tolerance, and life expectancy. In general, QOF investments are illiquid, meaning the money is inaccessible for some time. Further, if funds are withdrawn before the required holding periods, the Opportunity Zone benefits would be lost. Any gains that would be taxed at the 0% rate should probably be taken rather than deferred when they may be taxable. Real estate investors should compare the benefits of a QOZ investment with a Section 1031 exchange. Real estate investors with significant accumulated depreciation, who may not wish to leave real estate to their estate should consider this opportunity. As always, tax considerations are not the only considerations for investments, and investors should take into account the change in risk and expected return on their entire portfolios when considering any investment. Finally, gifting an interest in a QOF is an inclusion event, which ends the deferral and disqualifies further QOZ treatment. Leaving a QOF investment in an estate is not an inclusion event, but the QOF investments get a carry-over basis rather than a step-up in basis, and the gains are taxed at the end of the deferral period as they would have been to the decedent.[11] Appreciated property that is expected to be left to heirs is generally better held than sold and rolled into a QOF investment. (Proposed changes in estate tax law would change this, however.) Talk to a financial advisor to find out whether a Qualified Opportunity Zone investment is right for you.

Works Cited

Blank Rome LLP. (2020, January 13). IRS Publishes Final Opportunity Zone Regulations. Retrieved from JD Supra: https://www.jdsupra.com/legalnews/irs-publishes-final-opportunity-zone-99722/#:~:text=As%20a%20reminder%2C%20a%20%E2%80%9Csin,of%20alcoholic%20beverages%20for%20consumption

Economic Innovation Group. (2021, April 30). Opportunity Zones. Retrieved from Economic Innovation Group: https://eig.org/opportunityzones/facts-and-figures

HUD. (2021, 05 03). Opportunity Zones. Retrieved from hud.com: https://opportunityzones.hud.gov/

Internal Revenue Service. (2021 , April 30). FS-2020-13. Retrieved from www.irs.gov: https://www.irs.gov/newsroom/opportunity-zones

Internal Revenue Service. (2021, April 30). Opportunity Zone Frequently Asked Questions. Retrieved from IRS: https://www.irs.gov/credits-deductions/opportunity-zones-frequently-asked-questions

Internal Revenue Service. (2021, April 30). Opportunity Zones. Retrieved from www.irs.gov: https://www.irs.gov/credits-deductions/businesses/opportunity-zones

Levine, J. (21, August 2019). How Qualified Opportunity Zone Funds Create Unique Estate Planning Challenges For Beneficiaries. Retrieved from kitces.com: https://www.kitces.com/blog/qualified-opportunity-fund-qoz-qof-defer-capital-gain-estate-planning/

McCarter, C. (2020, February 25). The 2 Hidden Benefits fo Opportunity Zone Investing. Retrieved from OpportunityDb The Opportunity Zone Database: https://opportunitydb.com/2020/02/hidden-benefits-of-opportunity-zone-investing/

[1] (Internal Revenue Service, 2021)

[2] (Internal Revenue Service, 2021 )

[3] (Internal Revenue Service, 2021)

[4] (Blank Rome LLP, 2020)

[5] (HUD, 2021)

[6] (Economic Innovation Group, 2021)

[7] (Internal Revenue Service, 2021)

[8] (Internal Revenue Service, 2021)

[9] (McCarter, 2020)

[10] Every other hypothetical I’ve seen grows the capital gains for ten years but only subtracts out the value of the tax due in 2027 at the end of the analysis, incorrectly inflated the benefit of the QOF.

[11] (Levine, 21)