What You Need to Know About DSTs

Investing in Delaware Statutory Trusts (DSTs)

Summary:

Delaware Statutory Trusts (DSTs) allow gains on the sale of real estate to be reinvested in institutional grade, professionally managed real estate holdings while retaining tax deferral benefits under §1031. A 1031 exchange via a DST allows the transition of actively managed, concentrated real estate holdings, to a tax deferred, passive income stream with the potential for diversification. For the real estate investor who wants to improve diversification, reduce management demands, pass assets to heirs, or identify a backup property to a regular 1031 exchange, a DST is a useful tool in the toolbelt.

Background:

A trust, as defined by the IRS is “a relationship in which one person holds title to property, subject to an obligation to keep or use the property for the benefit of another”.[1] The Delaware Statutory Trust is a special type of trust established to hold real estate assets and qualifies as acceptable replacement property for deferral of capital gains taxes under §1031. The DST first came into existence in 1988 with the Delaware Statutory Trust Act. The IRS clarified their position on using a 1031 exchange in conjunction with a DST in Internal Revenue Ruling 2004-86 which states: “A taxpayer may exchange real property for an interest in the Delaware Statutory Trust described above without recognition of gain or loss under §1031, if the other requirements of §1031 are satisfied.”[2]

Delaware Statutory Trust Investments:

The DST structure can be used to purchase a wide variety of real estate investments including multifamily, medical, commercial, industrial, storage etc. A DST offering can be a single property such as an apartment building or consist of a portfolio of properties.

Some of the pros to using a DST for an investment vehicle include:

- Eligibility for 1031 exchange tax deferral.

- Diversification across property types, tenants, and geographic locations.

- Access to institutional grade real estate opportunities.

- No landlord responsibilities.

- Debt in a DST is nonrecourse to the individual investor. All other factors equal, the DST holding structure can lower an investor’s risk by eliminating recourse debt.

Some of the cons of using a DST for an investment vehicle include:

- Liquidity is limited until the underlying investment property is sold. The timing of a property sale is outside of the control of the individual investor. Typically, the time frame for a DST investment to go “full cycle” is 3-7 years.

- Fees may be higher than individual real estate investments when considering sponsor mark-up, management fees, disposal fees, etc.

- DSTs are only for accredited investors. An accredited investor is defined as an individual with:

- A net worth of $1,000,000 or more excluding primary residence.

- Annual income of $200,000 for an individual or $300,000 for a married couple for the last two years.[3]

- The minimum investment size in a DST is typically $100,000.

The Seven Deadly Sins of DSTs

Because of the substantial tax benefits related to DSTs, there are additional rules on the DST structure not relevant to other real estate holding structures. They are as follows:

- After a DST offering has closed, no additional contributions can be made.

- Loan terms cannot be renegotiated by the DST Trustee and new loans cannot be made except in very specific cases.

- Proceeds from the sale of real estate cannot be reinvested by the trustee.

- Improvements to properties held by a DST are limited to normal repairs and maintenance, minor improvements, and improvements required by law.

- Assets held by the DST for distribution can only be held as cash or short-term debt obligations.

- The DST must distribute all cash beyond necessary reserves.

- A DST trustee cannot make new or renegotiate current leases except in the case of tenant insolvency or bankruptcy. This is typically navigated by using a Master Lease Structure with a Master Tenant that subleases to other tenants.[4]

Where are the Properties Purchased by Delaware Statutory Trusts?

Individuals may see the name Delaware Statutory Trust and assume there are geographic restrictions on using the DST. The DST entity structure is based on Delaware law, but may be used to invest in real estate anywhere in the United States. International real estate is not eligible to be held in a DST.[5]

What can be Invested into a Delaware Statutory Trust (DST)?

Any proceeds from the sale of real estate eligible for 1031 exchange may be used in a DST and retain eligibility for 1031 exchange tax deferral status. A 1031 Exchange Qualified Intermediary is required for the completion of any 1031 exchange to avoid taking receipt of proceeds. Once an investor receives proceeds from the sale of real property, gains or losses are realized and an exchange is no longer possible.

An investor may also use “new money” to invest in a DST opportunity if the offering is appealing apart from tax deferral. Please note that a DST is regulated and sold as a security. To purchase a DST, an investor must work with a properly licensed securities professional.

What are the Tax Benefits of a Delaware Statutory Trust Investment?

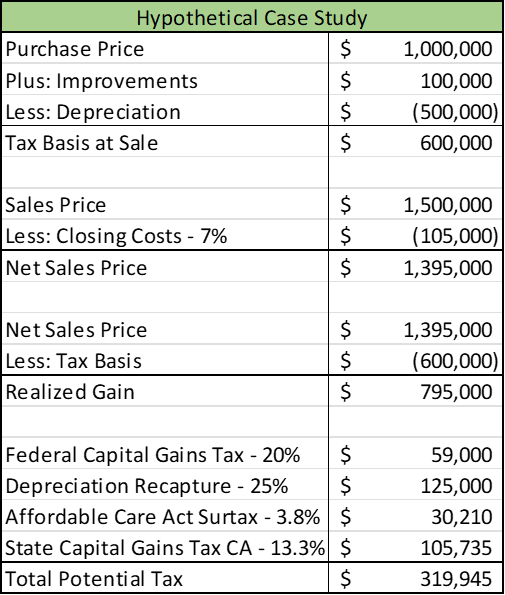

One of the most obvious benefits of the Delaware Statutory Trust is the ability to defer taxes from the sale of real estate via a 1031 exchange. The example below shows the potential tax savings from using a 1031 exchange and the net drag taxes can have on your returns compared to a tax deferral strategy. Note that the 1031 exchange can be used with or without a DST.

Source: Rothman Investment Management calculations.

Source: Rothman Investment Management calculations.

The above example assumes the investor is in the highest tax brackets for capital gains and has triggered the Affordable Care Act Surtax. For individuals converting actively managed real estate to a passive income stream, the DST has the potential to improve cash flow by preserving more funds for reinvestment. Please note that the above example is for illustration purposes only and does not constitute tax advice. Consult with your accountant or financial advisor for your specific tax situation.

Using the DST investment allows the opportunity to defer capital gains taxes indefinitely. In an ideal scenario where the basis in the investment is not needed to live, an investor can use the “swap until you drop” strategy to defer taxes until death. The investment gets a step up in basis at death allowing an investor to preserve more assets for heirs. This makes DST a valuable estate planning tool.

Who should consider Delaware Statutory Trusts?

The advantages of DSTs are primarily for those real estate investors interested in the tax deferral benefits. Additionally, DSTs should appeal to individuals seeking to reduce their time and effort spent on property management while retaining exposure to real estate as an asset class. After finalizing the sale of an investment property, a section 1031 exchange requires the exchange property to be identified within 45 days and closed on in 180 days. A DST can provide a good backup plan in case the purchase of the identified property fails, or the value is inadequate to offset the entire sale price of the original property.

The DST structure allows for smaller investments ($100,000) than may be required to purchase an entire property as an individual investor. This allows an investor to diversify across multiple real estate holdings via multiple DST opportunities.

The “swap until you drop” concept allows the DST to be an estate planning vehicle for those who wish to defer capital gains until the assets receive a step up in basis when passed to heirs. This is particularly useful when the investor does not want to hold their current investment property indefinitely.

The DST can also be used as a tax planning tool for individuals seeking to use the proceeds of a real estate sale over an extended period, such as in retirement. By investing smaller portions in multiple DSTs, taxpayers can take capital gains in smaller bites as DSTs go full cycle. This allows taxpayers to stay out of higher tax brackets and only pay taxes on gains as the funds are needed.

There are many issues to consider when evaluating the merits of a DST investment. These include: your liquidity needs, tax rate, risk tolerance, and life expectancy. In general, DST investments are illiquid, with the typical DST taking 3-7 years for a liquidity event to exit. Any gains that would be taxed at the 0% rate today should likely be taken rather than deferred to a later date when they may be taxable. Real estate investors should compare the benefits of a DST Section 1031 Exchange with the benefits of a Qualified Opportunity Zone (QOZ ) investment. Tax considerations are not the only considerations for investments, and investors should consider the change in risk and expected return on their entire portfolios when contemplating any investment. Talk to a financial advisor to find out whether a Delaware Statutory Trust investment is right for you.

Works Cited

Getty, P. M. (2017). Real Estate Tax Deferral Strategies Utilizing the Delaware Statutory Trust (DST).

Goodwin, D. (2021, March 21). Top 10 Reasons Real Estate Investors Are Jumping into DSTs. Retrieved from Kiplinger: https://www.kiplinger.com/real-estate/real-estate-investing/602456/top-10-reasons-real-estate-investors-are-jumping-into-dsts

Hayes, A. (2021, August 2021). Accredited Investor. Retrieved from Investopedia: https://www.investopedia.com/terms/a/accreditedinvestor.asp

Internal Revenue Service. (2017, September 27). Rev. Rul. 2004-86. Retrieved from Internal Revenue Service: https://www.irs.gov/irb/2004-33_IRB#RR-2004-86

Internal Revenue Service. (2022, February 17). Definition of a Trust. Retrieved from Internal Revenue Service: https://www.irs.gov/charities-non-profits/definition-of-a-trust#:~:text=In%20general%2C%20a%20trust%20is,which%20the%20organization%20is%20organized.

Meredith, D. (2020). The DST Revolution (2 ed.). La Jolla, California.

[1] (Internal Revenue Service, 2022)

[2] (Internal Revenue Service, 2017)

[3] (Hayes, 2021)

[4] (Meredith, 2020)

[5] (Getty, 2017)